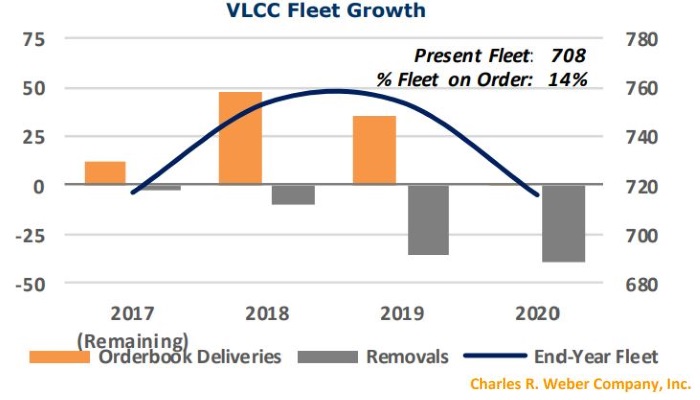

VLCC Cargoes Keep On Rising

Cargo availability is on the rise in the Middle East VLCC market, but rates don’t seem to be able to pick up considerably. In its latest weekly report, shipbroker Charles R. Weber said that “VLCC rates in the Middle East market posted a minor improvement this week, in‐line with a stronger pace of demand and recent demand strength in the West Africa market. A total of 23 fixtures were reported in the Middle East market, representing a 28% w/w gain. The West Africa market saw six reported fixtures, off by three w/w (though the four‐week moving average has risen to a one‐month high)”.

Accordin to CR Weber, “the immediate fundamentals facing the market remain poor: in the Middle East market, there are 31 units available to cover 3 remaining regional cargoes and four West Africa cargoes. The implied surplus of 24 units remains level with the view a week ago at a three‐month high; the surplus is twice the 12‐month average. As participants move into a September program, demand is expected to be busier on both seasonality (with a reduction of crude supply from Middle East producers to meet domestic summer demand surges subsiding) and geopolitical factors (as resolve by OPEC members to adhere to quotes appears to be waning as the strategy has failed to yield desired results). Any improvement in the demand profile however, will likely have little impact on rates, at very least while participants work early September cargoes, given the extent of surplus tonnage carrying over from August to September. Thereafter, the extent of early September demand and draws from the West Africa market will have a large baring on rate developments thereafter, as both of these can change the supply/demand positioning considerably”.

Middle East

According to the shipbroker in the Middle East, “AG‐FEAST rates pared last week’s losses, adding one point to conclude ws41. Corresponding TCEs rose by 18% to conclude at ~$12,088/day. Rates on the AG‐USG route via the Cape were unchanged at ws23. Triangulated Westbound trade earnings were off by 2% to ~$19,780/day”. In the Atlantic Basin, CR Weber said that “rates in the West Africa market lagged those in the Middle East with the WAFR‐ FEAST route shedding 2 points to conclude at ws48. Corresponding TCEs were off by 4% to ~$16,792/day. After last week’s gains in the Caribbean market, muted demand and further testing showed a slightly more ample supply fundamental, which lead to a paring of regional rates. The CBS‐SPORE route eased by $150k to conclude at $3.10m lump sum”.

In the Suezmax market, “demand in the West Africa Suezmax market was muted this week with just five fixtures reporting, representing a five‐month low. Despite this, rates received a modest boost following stronger than anticipated demand for coverage of August’s final decade, which left the position list slightly less overpopulated than previously expected. The WAFR‐UKC route added 2.5 points to conclude at ws67.5, accordingly. A moderating of VLCC coverage past August’s final decade shows greater demand prospects for Suezmaxes, which could help to keep rates stable, or possibly offer a small measure of fresh gains”, CR Weber said.

In the Aframax market, the shipbroker said that “a revised tally of last week’s Caribbean Aframax fixture activity pushed the four‐ week moving average to a four‐month high, enabling modest rate gains this week as demand levels remained relatively elevated. The CBS‐USG route added five points to conclude at ws90. Little substantial change is likely during the upcoming week”.

eanwhile, in the product tanker market, the shipbroker said that “the USG MR market observed a surge in rates this week after a fresh geographic diversification of trades in the Atlantic basin in recent weeks reduced available supply and demand increased this week. The weekly tally of regional fixtures jumped to an eight‐week high of 39, representing a w/w gain of 25%. Of this week’s tally, voyages to Europe accounted for just four (‐5, w/w) as traders scaled back interest in this direction following six consecutive weeks of above‐average demand; 22 fixtures were bound for points in Latin America and the Caribbean (+3, w/w) and the remainder are for alternative destinations or have yet to be determined. Rates on the USG‐UKC route surged 60 points to conclude at ws140 – the highest since late June. The USG‐CBS route added $275k to conclude at $625k lump sum (a four‐month high) and the USG‐CHILE route added $275k to conclude at $1.325m lump sum (a two‐month high)”.

CR Weber concluded that “this week’s gains were aided by a limiting of inbound tonnage to the USG earlier as ballast directions of units freeing at various parts of the western Atlantic basin were more diverse. However, with the USG market now offering a strong premium to all viable alternatives, we expect that a fresh buildup of positions will ensue during the upcoming week as the ballast orientation is now concertedly to the USG. Presently, the two‐week forward view of available tonnage shows 33 available units (11% fewer than a week ago). Charterers resistance is increasingly apparent at the close of the week and with more units expected to progressively appear during the upcoming week, we expect that modest downside at the start of the upcoming week will lead to a stronger correction by mid‐week, failing a strong extending of demand growth”